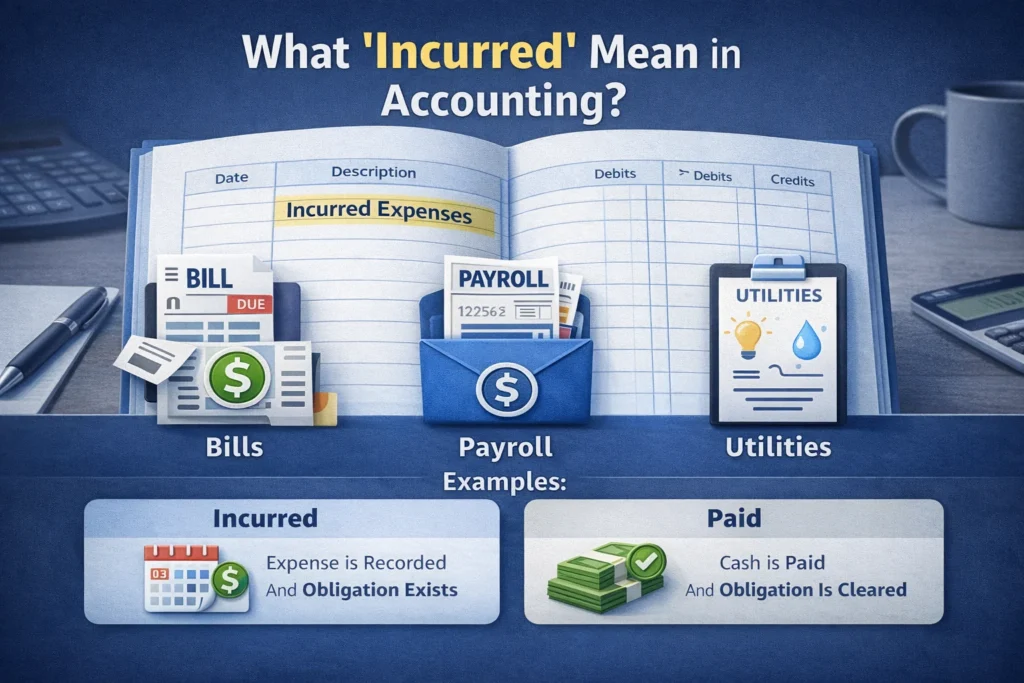

In accounting, “incurred” means that a company has become legally responsible for an expense or liability, regardless of whether it has paid the amount yet.

If you’ve ever reviewed financial statements, prepared a budget, or studied accounting, you’ve likely seen the word incurred. It appears frequently in income statements, balance sheets, and expense reports—but what does it actually mean?

Understanding the term “incurred” is essential for accurate bookkeeping, financial reporting, and business decision-making. You’re a student, small business owner, or finance professional, this guide will clearly explain what incurred means in accounting, how it works, and why it matters.

In simple terms:

An expense is incurred when the obligation happens not when the cash is paid.

Understanding “Incurred” in Simple Words

When a business incurs a cost, it means:

- The service has been received, or

- The goods have been delivered, or

- A legal obligation has been created

Payment may happen immediately or later. The key idea is responsibility, not cash flow.

For example:

- A company uses electricity in January but pays the bill in February.

The electricity expense is incurred in January. - A supplier delivers office supplies on credit.

The expense is incurred when the supplies are received.

Incurred vs Paid: What’s the Difference?

This is one of the most important accounting distinctions.

| Term | Meaning | Example |

|---|---|---|

| Incurred | Expense or obligation exists | January rent due |

| Paid | Cash has been transferred | Rent paid in February |

Under accrual accounting, expenses are recorded when incurred, not when paid.

Why “Incurred” Is Important in Accounting

The concept of incurred expenses supports two major accounting principles:

1. Accrual Accounting Principle

Expenses are recorded when they occur, not when payment is made.

2. Matching Principle

Expenses should be matched with the revenues they help generate.

For example:

If employees worked in December but are paid in January, the salary expense belongs to December because that’s when it was incurred.

Types of Costs That Can Be Incurred

Operating Expenses

- Rent

- Utilities

- Salaries

- Office supplies

These are incurred when services are used or goods are delivered.

Accrued Expenses

These are expenses incurred but not yet invoiced or paid.

Examples:

- Interest accumulating on a loan

- Wages earned but not yet paid

- Taxes owed

Capital Expenditures

If a business purchases machinery on credit, the cost is incurred when the asset is received—even if payment is delayed.

How Incurred Expenses Appear in Financial Statements

Income Statement

Expenses are recorded in the period they are incurred.

Example:

If a company generates revenue in March using raw materials purchased on credit, the material cost is incurred in March.

Balance Sheet

Unpaid incurred expenses appear as liabilities under:

- Accounts Payable

- Accrued Expenses

- Notes Payable

These represent obligations the company must settle.

Journal Entry Example for Incurred Expense

Suppose a company receives a $2,000 utility bill for December but will pay in January.

The journal entry in December:

Debit Utilities Expense $2,000

Credit Accounts Payable $2,000

This records the expense when it was incurred.

Real-Life Examples of “Incurred”

Example 1: Advertising Services

- A marketing agency runs ads in April.

- Invoice is issued in May.

- Payment is made in June.

The advertising expense is incurred in April.

Example 2: Loan Interest

- A company has a loan.

- Interest accumulates daily.

- Payment is made quarterly.

Interest is incurred daily, even if paid later.

Example 3: Employee Bonuses

- Employees earn performance bonuses in December.

- Bonuses are paid in January.

The bonus expense is incurred in December.

Incurred in Cash Accounting vs Accrual Accounting

| Accounting Method | When Expense Is Recorded |

|---|---|

| Cash Accounting | When paid |

| Accrual Accounting | When incurred |

Most large businesses use accrual accounting because it provides a more accurate financial picture.

Common Phrases Using “Incurred”

You may see:

- Expenses incurred

- Costs incurred

- Losses incurred

- Interest incurred

- Liabilities incurred

All refer to obligations that have arisen, whether or not payment has occurred.

Misconceptions About “Incurred”

Incurred means paid

False. Payment can happen later.

Only physical purchases are incurred

False. Services, interest, and taxes can also be incurred.

Incurred expenses always affect cash flow immediately

False. They affect accounting records first; cash flow changes when payment is made.

Why Businesses Track Incurred Expenses Carefully

- Accurate profit calculation

- Better budgeting and forecasting

- Tax compliance

- Improved financial transparency

- Stronger financial planning

Tracking incurred expenses ensures financial statements reflect true business performance.

Practical Tip for Business Owners

Always record expenses in the period they happen—even if the bill hasn’t arrived yet. This prevents overstating profits and avoids financial surprises later.

For example:

If you wait to record a large invoice until payment is made, you may temporarily show inflated profits.

FAQs

What does incurred mean in accounting?

It means a company has become responsible for an expense or liability, even if it has not yet paid the amount.

When is an expense considered incurred?

An expense is incurred when goods or services are received or when a legal obligation is created.

Is incurred the same as paid?

No. Incurred means the obligation exists. Paid means money has been transferred.

Does incurred apply only to expenses?

No. It can apply to liabilities, interest, taxes, and other financial obligations.

Why are incurred expenses important?

They ensure accurate financial reporting and align costs with the correct accounting period.

What is an accrued expense?

An accrued expense is an incurred expense that has not yet been paid or invoiced.

How does incurred affect profit?

It reduces profit in the period the expense is recorded, even if payment happens later.

Is incurred used in tax reporting?

Yes. Many tax systems require expenses to be recorded when incurred under accrual accounting rules.

Conclusion

The term “incurred” is a cornerstone of accounting. It ensures that businesses record expenses and obligations at the correct time when they actually happen not simply when cash changes hands.

From salaries and utilities to interest and taxes, recognizing incurred expenses provides a realistic view of financial performance.

In short, incurred means responsibility not payment and understanding this concept is vital for sound financial management.

Discover More Related Articles:

- Why Most Keywords Say “Not Provided” in Google Analytics in 2026

- RCV Meaning in Insurance: Replacement Cost Value Explained in 2026

Laura Jackson is a writer at textroast.com, where she creates engaging articles that decode the meanings behind slang, phrases, and everyday expressions. Passionate about language and communication, she makes complex or confusing terms easy to understand, turning learning into a fun and relatable experience for readers around the world.