Definition

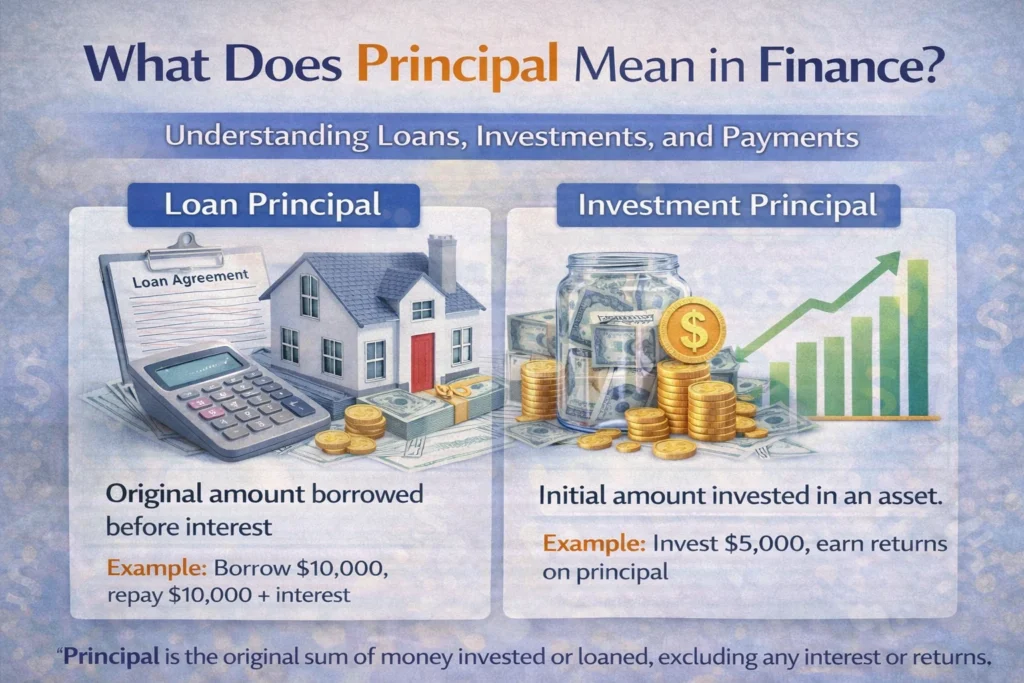

In finance, principal refers to the original sum of money that is invested, borrowed, or loaned, on which interest is calculated. In the context of loans, the principal represents the initial amount borrowed that must be repaid, while in investments, it is the initial amount invested before any returns or interest are earned.

In finance, the term principal comes up frequently, but its meaning is often misunderstood. Whether you’re dealing with loans, investments, or interest calculations, understanding what principal means is crucial for making informed financial decisions.

This article explains what principal means in finance, its different contexts, examples, and tips for managing principal amounts. We’ll also include FAQs to clarify common questions.

In simple terms, principal is the core amount of money before interest, gains, or fees are applied.

Understanding Principal in Finance

The principal is essentially the base amount of money you start with. It is separate from:

- Interest – the cost of borrowing or the earnings from an investment.

- Fees – additional charges applied to financial transactions.

Example:

- Loan: You borrow $10,000. That $10,000 is the principal. Interest accrues on this amount.

- Investment: You invest $5,000 in a fixed deposit. That $5,000 is your principal.

Knowing the principal is important because it affects how much interest you pay or earn over time.

Principal vs Interest

Principal and interest are closely related but different concepts:

| Term | Definition | Example |

|---|---|---|

| Principal | Original amount borrowed or invested | $10,000 loan or $5,000 investment |

| Interest | Money paid on the principal over time | $500 interest on a loan or $300 earned on an investment |

Interest is always calculated on the principal, either as a percentage of it (simple interest) or as part of a growing balance (compound interest).

Principal in Loans

In loans, the principal is the amount you actually borrow, excluding interest.

Example:

- Loan amount: $20,000

- Annual interest rate: 5%

- Loan term: 3 years

You owe $20,000 (principal), and interest will be calculated on this amount. Over time, as you make payments, the principal decreases.

Key Points:

- Loan payments often include both principal and interest.

- Early repayment reduces principal faster and saves interest.

- Different loan types (mortgage, personal loan, auto loan) all track principal.

Principal in Investments

In investing, the principal is the amount you initially invest in stocks, bonds, mutual funds, or deposits.

Example:

- You invest $10,000 in a bond.

- The bond earns 6% interest annually.

- Your principal remains $10,000, while interest or gains are calculated on it.

Importance:

- Knowing your principal helps track ROI (Return on Investment).

- Principal preservation is crucial for conservative investors.

Principal vs Balance

While principal refers to the original amount, balance refers to the current amount owed or held.

- Loan: Balance = Principal remaining + Accrued interest – Payments made

- Investment: Balance = Principal + Gains – Withdrawals

Example:

- Borrowed $10,000 principal

- Paid $2,000

- Remaining balance = $8,000 + interest

Principal in Mortgages

In mortgages, understanding principal is vital because:

- Mortgage payments reduce principal gradually.

- Interest is often higher in the early years because it is calculated on the larger principal.

- Paying extra towards principal can reduce total interest paid over the loan term.

Example:

- Home loan: $250,000 principal

- Interest rate: 4%

- Loan term: 30 years

Early payments mainly cover interest, but as principal decreases, interest costs decline.

How to Reduce Principal Faster

- Make extra payments on top of monthly installments.

- Refinance to a lower interest rate.

- Choose a shorter loan term.

- Avoid skipping payments, as unpaid interest can increase principal in some cases.

Reducing principal quickly saves money over the long term.

Principal in Compound Interest

Compound interest is calculated on both principal and accumulated interest.

Example:

- Principal: $5,000

- Annual interest rate: 5%

- Time: 3 years

Calculation (compound interest formula):A=P(1+r/n)nt

Where:

- A = total amount after interest

- P = principal

- r = annual interest rate

- n = number of times interest is compounded per year

- t = number of years

After 3 years, the principal grows with compounded interest, showing the importance of the initial amount.

Principal in Bonds

In bonds, the principal is called the face value or par value.

- You invest in a bond for $1,000 (principal).

- The bond pays periodic interest (coupon) on the principal.

- At maturity, the issuer returns the principal.

Bonds rely on principal preservation and predictable returns.

Practical Tips for Managing Principal

- Track your principal separately from interest.

- Prioritize paying down principal in loans.

- Understand how principal affects interest calculations.

- For investments, protect principal to reduce risk exposure.

- Review loan and investment statements to see principal changes over time.

Examples Table: Principal in Different Contexts

| Context | Principal | Interest | Outcome |

|---|---|---|---|

| Personal Loan | $10,000 | $500 | Total owed = $10,500 |

| Mortgage | $250,000 | $40,000 | Payments reduce principal over 30 years |

| Bond | $1,000 | $50/year coupon | Principal returned at maturity |

| Investment | $5,000 | $300 earned | Principal + interest = $5,300 |

Common Misconceptions

- Principal is not interest. Principal is the base, interest is extra.

- Principal does not always stay the same. Loan principal decreases with payments; investments may grow.

- High principal doesn’t always mean high risk. Proper management ensures control.

FAQs

What does principal mean in finance?

It is the original amount of money borrowed, invested, or loaned, on which interest or returns are calculated.

Is principal the same as balance?

No. Balance includes principal plus interest and fees, minus payments made.

How is principal different from interest?

Principal is the original amount, while interest is the cost of borrowing or earning on that amount.

Can you pay only principal on a loan?

Yes, paying extra principal reduces the remaining balance and total interest owed.

Why is principal important in investments?

It is the starting amount, which determines future earnings and returns.

Does principal include fees?

No, principal is separate from fees or charges applied to loans or investments.

How do you calculate interest on principal?

Interest = Principal × Interest Rate × Time (for simple interest). Compound interest uses principal plus accumulated interest.

Can principal change over time?

Yes, in loans it decreases with payments; in investments, it may increase with additional deposits.

Conclusion

Understanding principal in finance is critical for anyone managing money, whether borrowing, investing, or saving. It is the foundation for calculating interest, tracking loan repayments, and assessing investment growth.

By focusing on principal, you can make smarter financial decisions, reduce costs, and maximize returns over time. Principal is the backbone of financial literacy knowing it empowers you to control your finances confidently.

Discover More Related Articles:

- REO Homes Explained: Benefits and How to Purchase Them in 2026

- Real Estate Conveyance Explained: Everything You Need to Know in 2026

Laura Jackson is a writer at textroast.com, where she creates engaging articles that decode the meanings behind slang, phrases, and everyday expressions. Passionate about language and communication, she makes complex or confusing terms easy to understand, turning learning into a fun and relatable experience for readers around the world.